The Economic and Investment Implications of Zombie Companies

How Debt-Dependent Firms Impact Productivity, Market Dynamics, and Bond Investors

Introduction

The rise of zombie companies—businesses that can pay interest on their debt but not the principal—poses significant challenges and distortions to the economy. These firms, unable to sustain operations without continuous external support, have proliferated due to factors like low interest rates and economic policies favoring debt accumulation.

The central question this article addresses is: What are the implications of zombie companies on economic productivity, market dynamics, financial stability, and bond investors? As interest rates rise and financing costs increase, zombie firms face growing pressures, potentially impacting the broader economy. For bond investors, the increased default risk and potential mispricing in the high-yield bond market are of particular concern. The article explores the need for reforms in insolvency regimes and stricter financial discipline to reduce the prevalence of these unproductive firms, ultimately aiming to enhance economic growth and stability while safeguarding investor interests.

Definition of Zombie Companies: Insights from Goldman Sachs

A zombie company is a business that generates enough income to pay the interest on its debt but is unable to repay the principal without resorting to external sources, such as shareholders, for additional cash. These companies are often characterized by their inability to cover their interest expenses from their operating profits over an extended period.

Goldman Sachs Research analysts Michael Puempel and Ben Shumway argue that traditional metrics used to identify zombie companies often include high-growth technology firms. These companies are typically young, and investors expect them to achieve high earnings in the future. Rather than nearing the end of their lifespan, these firms are seen as having significant potential.

Therefore, a more widely accepted measure of a zombie firm is one with an interest coverage ratio below one for three consecutive years, particularly for companies that have been operating for more than a decade. This measure helps to more accurately identify companies that are genuinely struggling to sustain their operations without continuous external support.

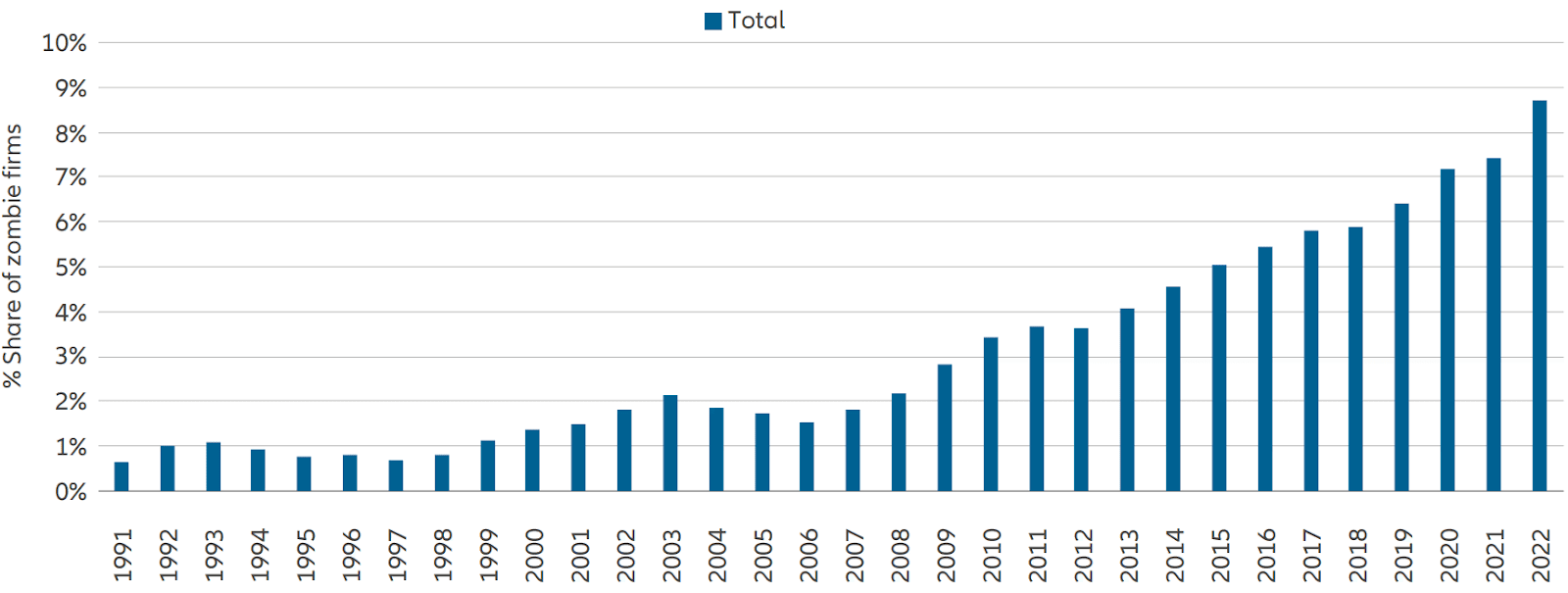

Historical and Economic Background on the Rise of Zombie Firms and Their Impact

Zombie firms have proliferated due to various factors, including political pressure and economic policies. Historically, Japanese banks engaged in "ever-greening," lending to insolvent borrowers to avoid recognizing losses, especially in the late 1990s and early 2000s. This practice kept unproductive firms afloat, preventing market restructuring and innovation. Similarly, in Europe and the US, low interest rates and quantitative easing (QE) have enabled private equity firms to acquire and heavily leverage retailers, fostering an environment conducive to the rise of zombie companies.

Market Distortion and Productivity Impact

The presence of zombie firms distorts market dynamics by lowering prices, raising wages, and congesting markets, thereby reducing overall productivity. These firms also prevent the process of "creative destruction," where inefficient businesses are replaced by more productive ones. The existence of zombie firms can temporarily soften the impact of economic downturns on employment but ultimately hampers job creation and economic growth by preserving inefficient operations.

Resource Misallocation and Economic Stagnation

The proliferation of zombie firms has led to significant congestion effects, draining resources from profitable companies and distorting competition. By holding onto capital, labor, and other resources, zombie firms prevent these assets from being used by more efficient and innovative companies. This misallocation of resources stifles new business development and technological advancements, reducing the overall dynamism and competitiveness of the economy. As a result, zombie firms not only impede productivity growth but also limit the potential for higher wages and better employment opportunities that could arise from more efficient firms.

Economic and Financial Stability Concerns

This congestion effect exacerbates economic stagnation, as thriving companies struggle to expand due to the scarcity of available resources. The persistence of zombie firms, therefore, creates a drag on economic vitality and perpetuates inefficiencies across various sectors. This has raised concerns about financial stability, especially as rising interest rates threaten to increase defaults among heavily indebted companies. The potential for a sudden wave of business closures could spike unemployment and disrupt economic sectors dependent on these struggling firms, posing a significant risk to the broader economy.

Impact on Monetary Policy Transmission

Zombie firms significantly impact the transmission of monetary policy to nonfinancial firms. Albuquerque and Mao's study, "The Zombie Lending Channel of Monetary Policy," shows that tighter monetary policy results in more favorable credit conditions for zombie firms compared to non-zombies. This allows zombie firms to reduce investment and employment less drastically, as banks restructure loans to avoid realizing losses, indicative of evergreening practices. This behavior contrasts with the traditional expectation that zombie firms, being more reliant on bank debt, would face stronger financial constraints. Consequently, zombie lending alters the effectiveness of monetary policy, particularly during tightening phases, by disproportionately benefiting unviable firms. To mitigate these distortions, the authors recommend strengthening bank balance sheets, limiting risky behavior, and improving insolvency regimes, ensuring monetary policy supports overall economic health.

Headwinds for Zombie Companies and Their Potential Impact

Zombie companies are currently facing three significant challenges:

Increasing Interest Rates: Central banks are raising interest rates to tackle persistent inflation. This action reduces aggregate demand, leading to lower revenues for many firms, and consequently, less cash available for zombie companies to pay down their debt.

Rising Financing Costs: These firms were already struggling to meet interest payments when rates were low. The increase in financing costs will only worsen this issue.

Diminished Appeal to Lenders: Banks and credit investors find lending to zombie companies less attractive now, as they can achieve better returns by lending to higher-quality firms at higher interest rates.

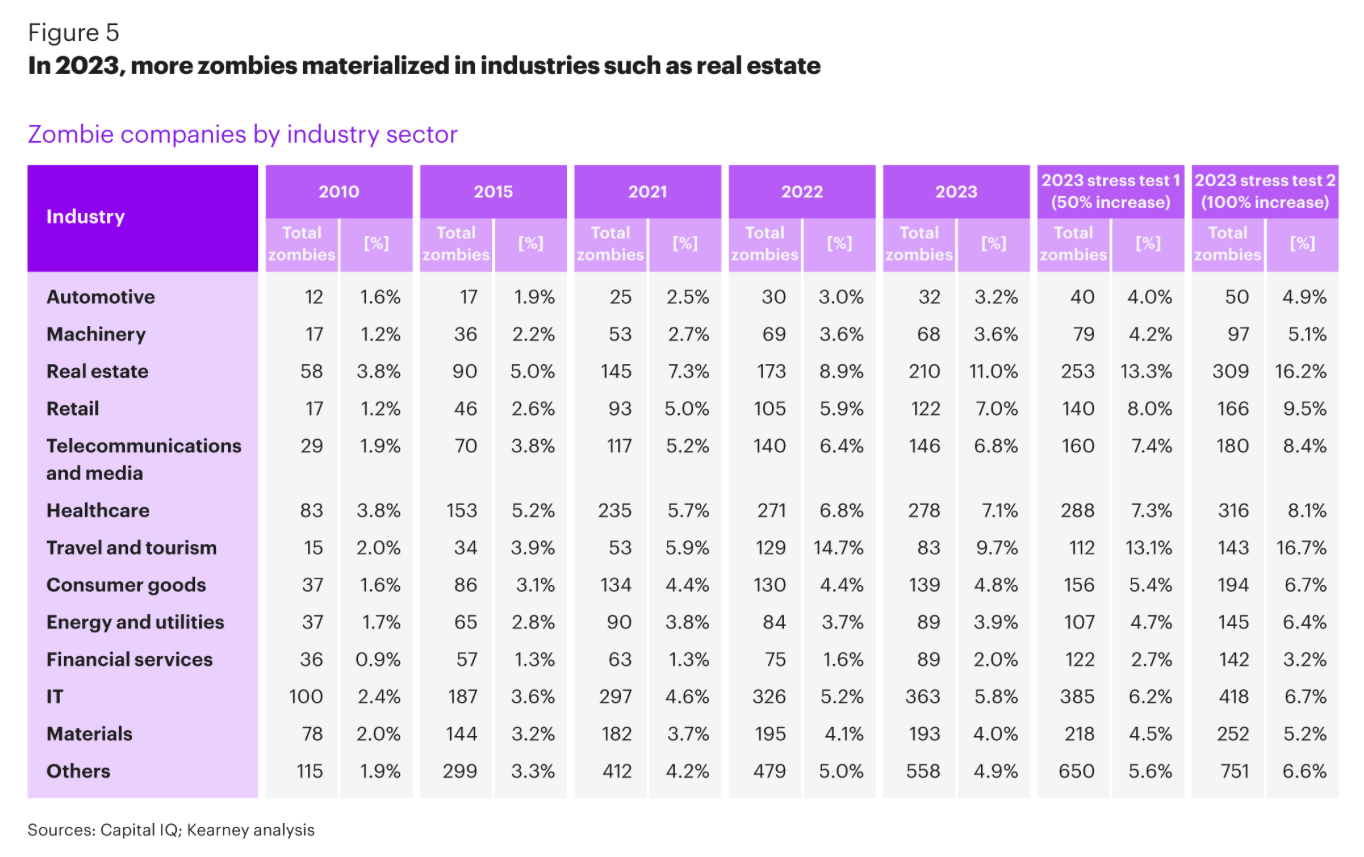

Defensive sectors, especially healthcare, have seen significant credit rating downgrades this year and have a higher proportion of zombie companies compared to cyclical sectors. This can be explained by stricter financing discipline in cyclical sectors and their ability to generate higher operating profits during economic booms, providing a buffer during downturns.

Economic "Spring Cleaning" and Investor Concerns

It is argued that any support should focus on companies with long-term viability, allowing zombie or non-profitable firms to go bankrupt to make room for stronger ones. Fiscal stimulus aimed at preventing defaults could result in inflation and a structural stagflation scenario, ultimately delaying the inevitable and hurting all economic agents.

Despite the bleak outlook, this scenario could be viewed as economic "spring cleaning." The collapse of weaker zombie companies could pave the way for more efficient firms, potentially leading to a stronger economy. However, a wave of defaults could alarm investors, especially given the shift of risky debt to less transparent private markets. This uncertainty might drive investors to seek higher yields on corporate loans, further increasing financing costs and potentially causing more defaults. Although the Federal Reserve might cut interest rates, it may not be enough to offset the negative impact of tighter financing conditions, creating a challenging environment for stocks.

Insolvency Regimes as a solution to Zombie Firms

A study comparing insolvency regimes across countries like the UK, US, Japan, and Germany highlights 13 key features affecting effectiveness: personal costs, restructuring barriers, court involvement, employee rights, SME procedures, discharge time, asset exemptions, preventative measures, new financing priority, cram-down on creditors, management dismissal, and creditor initiation.

High personal costs and barriers to restructuring discourage entrepreneurship and prolong insolvency processes. Excessive court involvement can slow down proceedings and increase costs, while strong employee rights may complicate restructuring efforts. Special procedures for SMEs and shorter discharge times facilitate quicker resolutions and a faster return to economic activity. Preventative measures and high priority for new financing support successful restructuring, and cram-down on creditors enables more efficient agreements. Mandatory dismissal of management ensures fresh leadership but may disrupt continuity, and allowing creditors to initiate proceedings provides a check on management but risks premature insolvency declarations.

Reforming insolvency regimes to reduce restructuring barriers and lower personal costs for entrepreneurs can mitigate the prevalence of zombie firms. This would improve capital allocation and spur productivity growth, addressing the productivity slowdown observed in many OECD economies. Efficient insolvency regimes ensure that resources are reallocated to more productive uses, enhancing overall economic productivity and reducing the negative impact of zombie firms on the economy.

Characteristics of Zombie Bonds

Investment Risks and Ratings of Zombie Companies

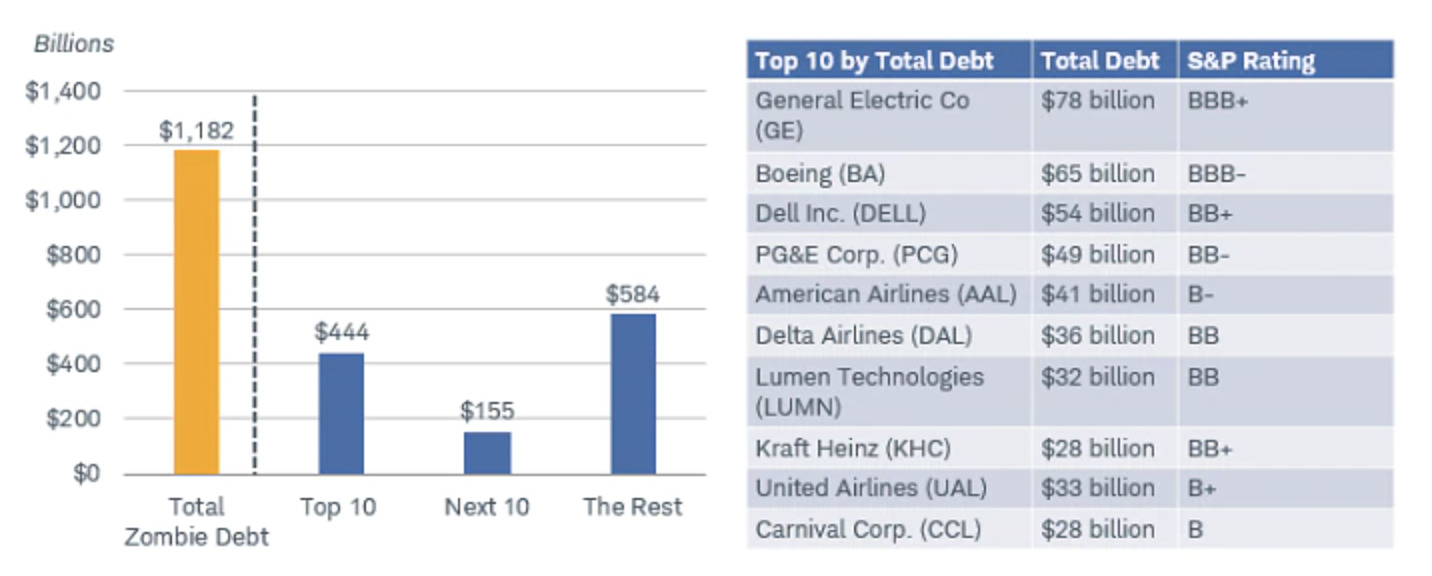

Zombie companies are generally unrated and unlikely to be included in funds, as they typically lack publicly traded debt. Those with ratings usually hold sub-investment-grade or "junk" ratings. Only 25 have investment-grade ratings of "BBB" or higher, while 137 have high-yield ratings. Although this reduces the immediate risk to individual investors, it highlights that the rated zombies—more likely to be held in mutual funds or ETFs—pose significant risk. Despite their numbers, a small group of zombie corporations has issued most of the debt. Investment-grade zombies facing downgrades to junk status could force fund houses to sell off these bonds, disrupting price stability.

Concentration of Zombie Debt and Market Risk

The amount of zombie debt is highly concentrated, with the top 10 issuers accounting for about 38% of all zombie debt. This concentration means the market risk is more about a few zombies with large amounts of debt rather than the sheer number of zombies. Therefore, diversification is crucial when investing in corporate or high-yield bonds.

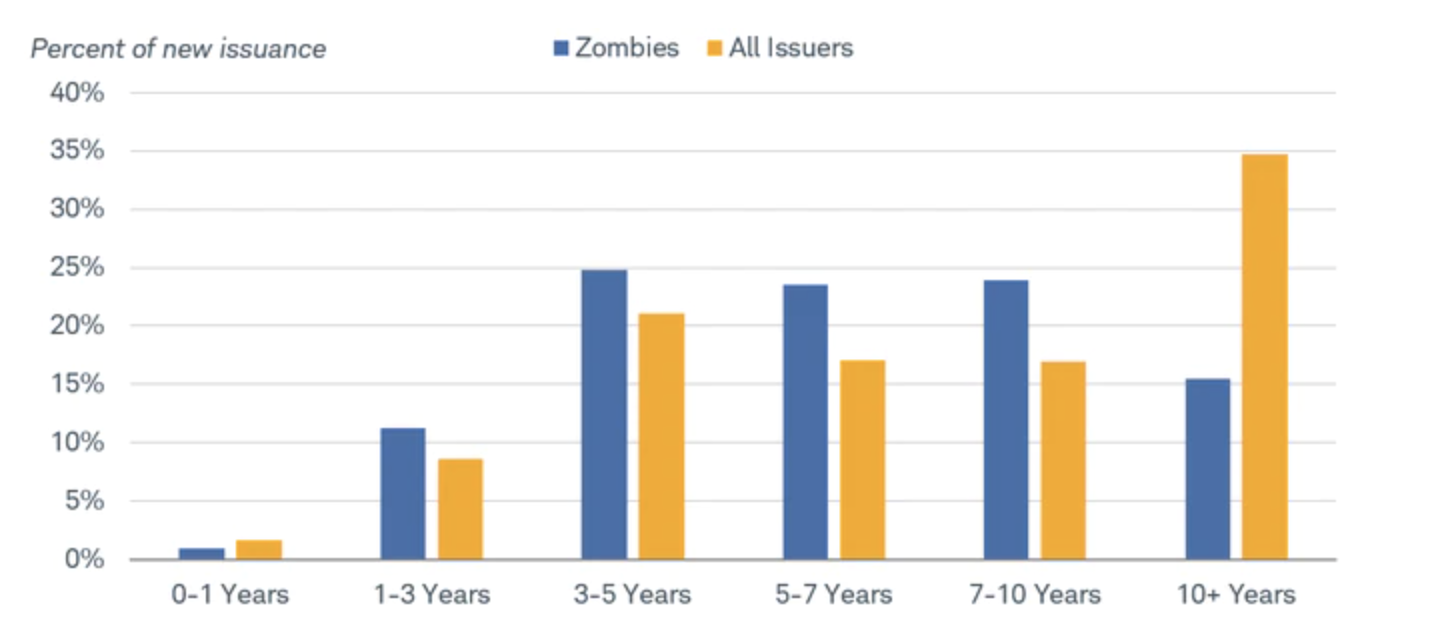

Rare occurrence of long term debts

Zombies have not issued as much long-term debt as rest of the corporate universe due to refinancing risk

Implication to individual investor

Increased Default Risk

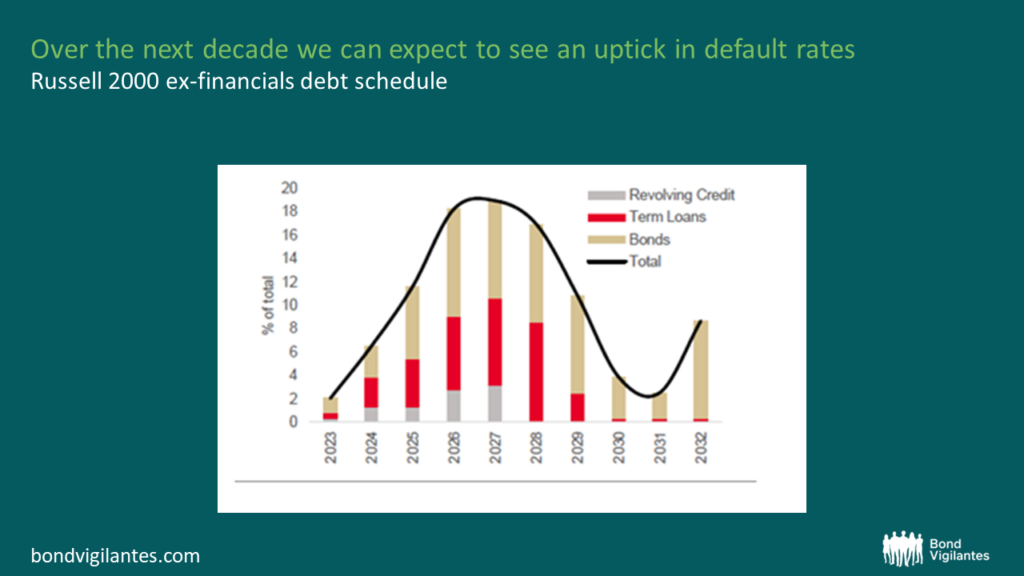

Given the current economic environment and rising interest rates, the default rate among zombie companies is expected to increase. These companies often survive on low-cost debt and may struggle to refinance or service their obligations under tighter monetary conditions. As a result, individual investors holding bonds from these companies face a heightened risk of default.

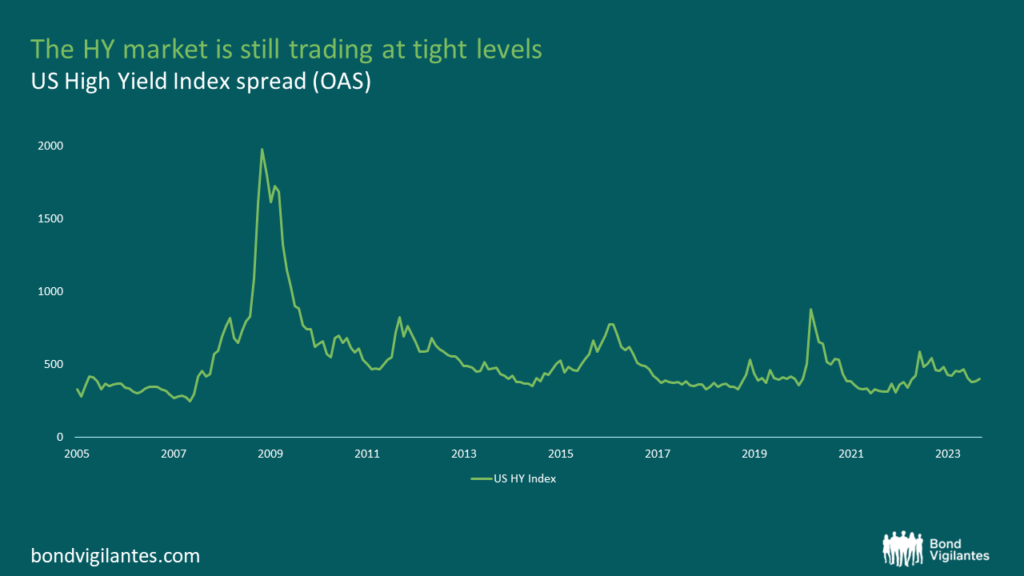

Mispriced High-Yield Bond Market

Despite the looming threat, the high-yield bond market does not fully reflect the risks associated with zombie companies. The optimism surrounding potential Federal Funds Rate (FFR) cuts has led to tighter spreads in the high-yield market, suggesting a degree of complacency among investors. This mispricing could result in significant losses if the anticipated rate cuts do not materialize, or if economic conditions worsen, leading to a wave of defaults.

Sector-Specific Caution

Investors should be particularly cautious in sectors where zombie companies are prevalent. These sectors are more vulnerable to economic downturns and shifts in interest rates, making them riskier investments. For example, industries that rely heavily on debt financing, such as energy, retail, and certain technology sectors, may have a higher concentration of zombie companies. Individual investors should conduct thorough due diligence and consider the financial health of companies within these sectors before investing.

References:

The Zombie Lending Channel of Monetary Policy, WP/23/192, September 2023

Zombie Firms: Navigating the Looming Threat of Higher Interest Rates - Bond Vigilantes

The rise of zombie companies – what are they and can they be stopped? | Hargreaves Lansdown

The walking dead: how the rise of zombie firms is affecting the global economy | World Finance

Economic Insights - Rising defaults: "zombie firms" will be the first to fall

沒有留言:

發佈留言